Volatility, Valuations, and Staying Grounded

There’s an old story about a farmer who, year after year, planted his crops regardless of the weather forecast. Some seasons brought rain. Others brought drought. Some years produced abundance, and others required patience.

When asked why he didn’t change his approach based on what he heard about the coming season, he simply replied, “I don’t farm based on the forecast. I farm based on what I know works over time.”

Investing often feels similar. There will always be forecasts—about markets, interest rates, geopolitical conflict, or the next downturn. Some will be right, many will be wrong. But long-term success has never come from reacting to every forecast. It comes from following a disciplined process that is built to endure through all seasons.

Over the past few weeks, we’ve had a number of conversations with clients asking a similar question: “What’s going on in the markets right now?” It’s a fair question—and one worth stepping back to answer with clarity.

A Volatile Start to the Year

Markets have experienced a meaningful pullback to start 2026. After reaching highs in late January, the S&P 500 declined roughly 7%–9% at its recent lows before stabilizing into the end of March. This represents a normal, though uncomfortable, correction following a strong prior run.

Volatility has been driven by several factors: shifting expectations around interest rates, continued concentration in certain areas of the market, and growing geopolitical uncertainty—particularly surrounding Iran and energy markets.

While these movements can feel significant in the moment, they remain well within the range of typical market behavior during a cycle.

Iran, Oil, and the Ripple Effect on the Economy

The situation with Iran has added another layer of uncertainty, primarily through its impact on oil prices. When oil prices rise, the effects extend well beyond energy markets—impacting transportation, manufacturing, and ultimately the cost of goods and services across the economy.

Higher energy prices can weigh on consumer confidence and spending, which is why markets tend to react quickly to these developments.

That said, the U.S. economy is structurally different than it was in past decades. The United States is now a net exporter of energy, which helps reduce the overall economic impact of rising oil prices compared to previous cycles. While higher oil still creates headwinds, it is less likely to derail growth on its own.

The Economy: Resilient Despite Headwinds

Even with these pressures, the underlying economy continues to show resilience.

- GDP growth has moderated but remains positive, with ~2% full-year growth in 2025.

- Inflation has cooled significantly from prior peaks, though it remains slightly above the Fed’s long-term target.

- The labor market has softened modestly, with unemployment around 4.4%, but remains stable overall.

- Consumer activity continues to hold up, even as confidence reflects a more cautious outlook.

This combination—moderating growth, cooling inflation, and stable employment—is consistent with a late-cycle, but still expanding, economy.

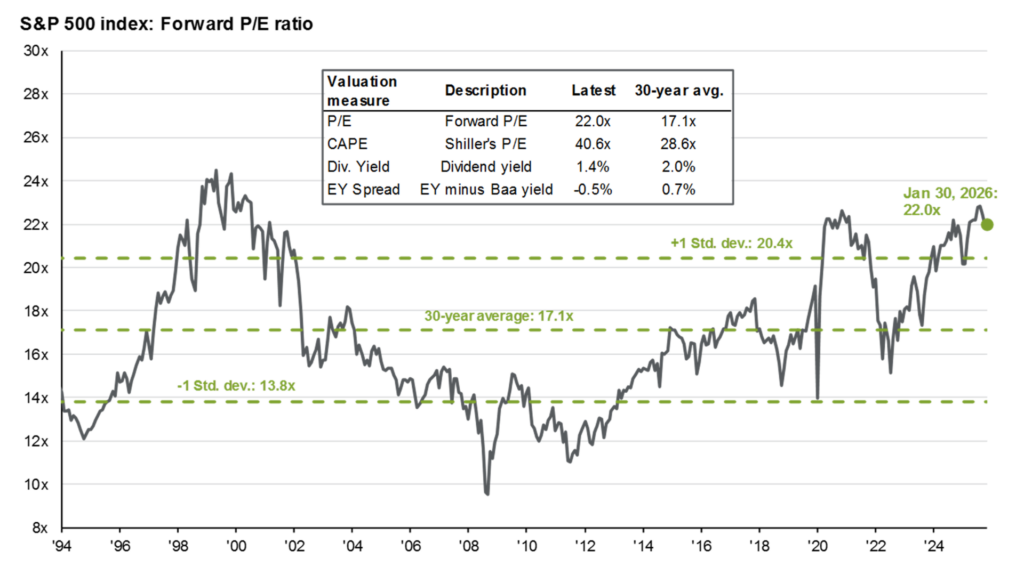

Valuations: Still Elevated, but Improving

The chart below from J.P. Morgan highlights an important dynamic in today’s market:

4

As of late March:

- The S&P 500 forward P/E is approximately 19.2x, compared to a 30-year average of 17.2x

- Valuations remain above historical norms, but are lower than they were just a few months ago

This improvement has come from a combination of market pullback and continued earnings growth.

For long-term investors—those with a 7+ year time horizon or longer—this level of valuation is not uncommon and should not be a primary driver of decision-making.

However, for those with shorter time horizons, or those relying on near-term withdrawals, elevated valuations reinforce the importance of proper allocation, risk management, and disciplined income strategies.

Not All Equities Are Created Equal

Another important takeaway from recent months is that leadership within the market is evolving.

In more volatile environments—especially when rates remain elevated and economic uncertainty increases—there can be meaningful advantages in:

- Companies with strong balance sheets

- Consistent cash flow

- Dividend-paying stocks

This is particularly relevant for clients in the Strategic Income Phase (Phase III), where reliability of income and preservation of capital play a larger role.

At the same time, it is important to remember that market leadership can shift quickly. Rotation does not always persist, and no single segment of the market consistently outperforms in all environments.

This is why diversification across strategies—and across SIG’s investment buckets—remains critical.

What Should Clients Do Right Now?

In moments like this, the temptation is to react—to adjust portfolios, move to cash, or try to anticipate what happens next.

But history consistently shows that long-term success is not driven by reacting to short-term volatility. It is driven by staying aligned with a well-constructed plan.

For most clients, the right next step is not a market decision—it’s a planning conversation:

- Are your investments aligned with your time horizon?

- Do you have the appropriate reserves in place?

- Is your income strategy positioned to weather volatility if needed?

If those answers are yes, then your plan is already doing exactly what it was designed to do.

If you’re unsure, or if it has been a while since your last review, this is a great time to connect with your SIG Financial Planner.

Staying Focused on What Matters Most

Markets will continue to move. Headlines will continue to change. There will always be a new reason to feel uncertain in the short term.

But the principles that drive long-term success remain remarkably consistent: discipline, patience, diversification, and a clear plan.

At Strategic Income Group, our mission remains unchanged:

Empowering individuals to live their best lives and leave a lasting legacy of financial security and positive impact.

And in environments like this, that mission matters more than ever.

References

- U.S. Bureau of Economic Analysis (BEA) – GDP and economic data

- U.S. Bureau of Labor Statistics (BLS) – Employment and inflation data

- The Conference Board – Consumer confidence and leading indicators

- J.P. Morgan Asset Management – Guide to the Markets (valuation data)

- U.S. Energy Information Administration (EIA) – U.S. energy production and export data

Compliance Disclosures

This commentary is provided for informational and educational purposes only and should not be construed as investment, tax, or legal advice. The views expressed reflect market and economic conditions as of the date noted and are subject to change without notice. Past performance is not indicative of future results. All investing involves risk, including possible loss of principal. Diversification and asset allocation do not guarantee a profit or protect against loss in declining markets.

Strategic Income Group is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training. For additional information, please refer to our Form ADV available at www.adviserinfo.sec.gov.